Volatility Update

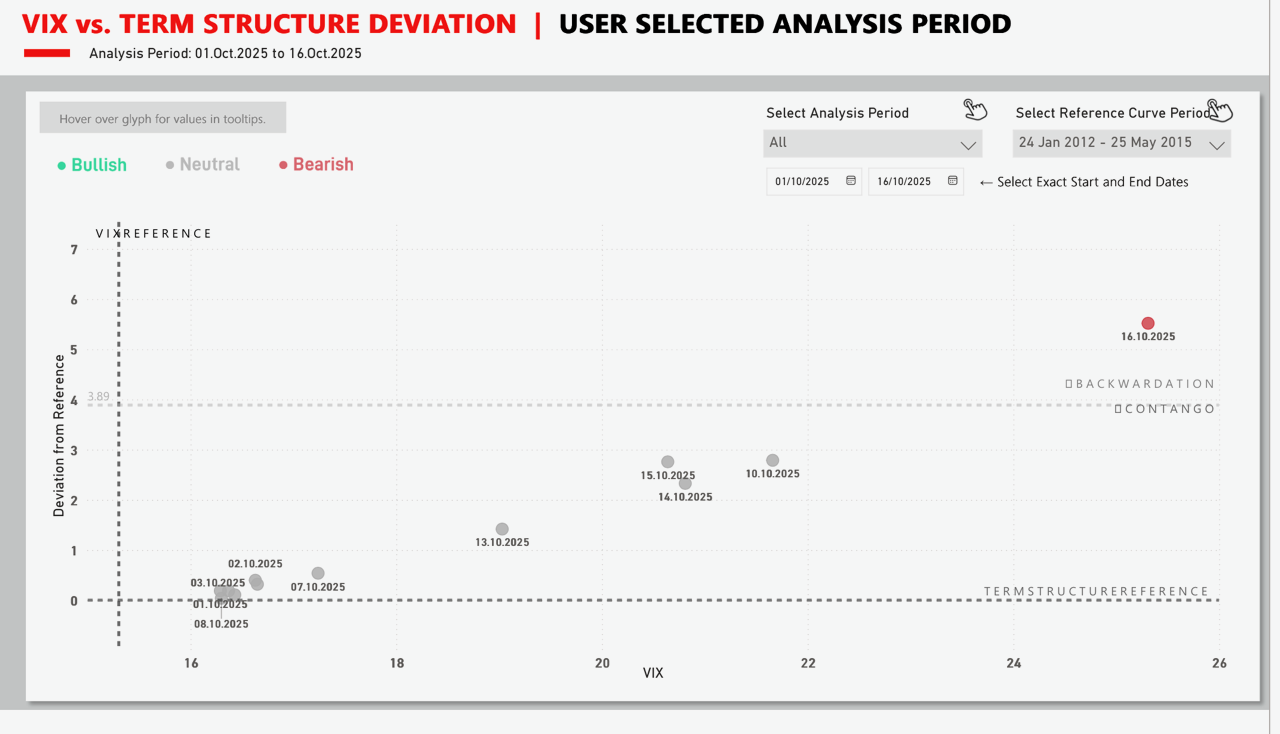

Following a period of elevated VIX in the first week of October (shown by the cluster of dots on lower right) — indicating higher degree of short-term risk — this concern has now spread to the longer term through a flattening of the slope of the term structure (dots to the right). VIX futures have now moved to backwardation implying that risk factors, whatever they are, may be perceived to be more of a longer-term nature.

This isn’t mere market turbulence—it signals a sentiment shift. What began as a short-term spike in volatility is now evolving into a broader concern. The transition from transient fear to sustained unease is evident in the flattening term structure and emergence of backwardation.

This shift demands strategic recalibration:

- Rebalancing toward defensive sectors that can weather prolonged uncertainty

- Extending hedges across longer durations to account for persistent volatility

- Reevaluating risk models that rely on mean reversion, as traditional assumptions may no longer hold

This illustration is for educative purposes only. If you have any questions or seek clarification please feel free to contact me at info@skmarketisghts.com

Sowmi Krishnamurthy CMT

SK Market Insights Ltd